Home Equity Loan Benefits: Why It's a Smart Financial Move

Home Equity Loan Benefits: Why It's a Smart Financial Move

Blog Article

Key Elements to Take Into Consideration When Applying for an Equity Financing

When thinking about applying for an equity lending, it is crucial to browse via numerous crucial variables that can dramatically affect your financial well-being. Comprehending the types of equity finances offered, evaluating your qualification based on monetary factors, and very carefully taking a look at the loan-to-value ratio are essential first steps.

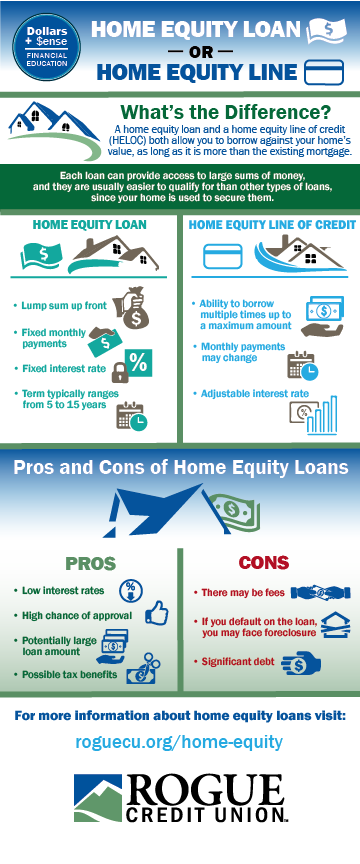

Types of Equity Loans

Numerous financial establishments provide a series of equity loans customized to meet varied loaning requirements. One usual type is the traditional home equity loan, where house owners can borrow a lump amount at a fixed rate of interest, utilizing their home as security. This sort of funding is optimal for those that need a huge sum of money upfront for a details function, such as home improvements or debt loan consolidation.

An additional popular choice is the home equity credit line (HELOC), which functions a lot more like a charge card with a rotating credit limitation based upon the equity in the home. Consumers can draw funds as needed, up to a specific restriction, and just pay rate of interest on the quantity utilized. Equity Loans. HELOCs appropriate for recurring expenses or jobs with unclear prices

Additionally, there are cash-out refinances, where property owners can refinance their current home mortgage for a greater quantity than what they owe and obtain the distinction in cash money - Alpine Credits Canada. This sort of equity lending is useful for those seeking to take benefit of reduced rates of interest or accessibility a large amount of cash without an additional monthly payment

Equity Finance Qualification Variables

When considering qualification for an equity lending, banks generally analyze variables such as the candidate's credit rating, revenue security, and existing financial obligation responsibilities. A crucial aspect is the credit rating rating, as it mirrors the debtor's creditworthiness and ability to repay the finance. Lenders like a higher credit history, typically over 620, to alleviate the danger related to lending. Earnings security is another essential aspect, showing the customer's capability to make routine car loan payments. Lenders might require proof of constant income via pay stubs or tax returns. Additionally, existing financial debt obligations play a considerable role in establishing eligibility. Lenders evaluate the debtor's debt-to-income ratio, with reduced proportions being more desirable. This ratio shows just how much of the consumer's revenue goes towards paying back debts, influencing the lender's decision on loan approval. By meticulously assessing these aspects, banks can figure out the candidate's eligibility for an equity loan and develop ideal car loan terms.

Loan-to-Value Proportion Factors To Consider

A reduced LTV ratio indicates much less danger for the lender, as the debtor has more equity in the property. Lenders normally favor lower LTV ratios, as they offer a higher cushion in situation the debtor defaults on the finance. A higher LTV proportion, on the other hand, recommends a riskier investment for the lending institution, as the customer has much less equity in the residential or commercial property. This might lead to the lending institution imposing greater rates of interest or stricter terms on the funding to mitigate the raised official statement threat. Customers need to aim to keep their LTV proportion as low as feasible to boost their possibilities of authorization and secure much more favorable funding terms.

Rate Of Interest and Costs Comparison

Upon examining interest prices and fees, debtors can make enlightened decisions concerning equity loans. Interest rates can substantially influence the total cost of the car loan, impacting monthly settlements and the complete amount settled over the loan term.

Besides rate of interest, debtors must additionally take into consideration the numerous costs linked with equity loans - Alpine Credits. These fees can include origination fees, appraisal charges, closing expenses, and early repayment fines. Source costs are billed by the lending institution for refining the loan, while evaluation costs cover the cost of assessing the residential property's worth. Closing expenses include different fees related to completing the finance arrangement. If the debtor pays off the loan early., early repayment fines might apply.

Settlement Terms Examination

Effective evaluation of settlement terms is important for borrowers looking for an equity finance as it directly impacts the funding's cost and financial end results. When evaluating settlement terms, debtors ought to meticulously review the loan's period, monthly settlements, and any possible penalties for very early settlement. The funding term refers to the length of time over which the consumer is expected to settle the equity car loan. Much shorter car loan terms typically lead to higher regular monthly settlements but reduced total rate of interest prices, while longer terms offer lower month-to-month payments however might lead to paying more rate of interest with time. Customers require to consider their economic circumstance and objectives to establish the most appropriate settlement term for their demands. In addition, understanding any fines for very early repayment is vital, as it can impact the adaptability and cost-effectiveness of the lending. By completely examining settlement terms, consumers can make informed decisions that line up with their monetary goals and make certain effective loan management.

Verdict

In final thought, when getting an equity car loan, it is essential to consider the sort of financing readily available, qualification elements, loan-to-value ratio, passion prices and fees, and repayment terms - Alpine Credits. By meticulously reviewing these vital aspects, debtors can make educated decisions that straighten with their monetary goals and circumstances. It is crucial to completely research study and compare alternatives to guarantee the very best feasible result when seeking an equity loan.

By thoroughly evaluating these aspects, financial institutions can establish the applicant's qualification for an equity finance and establish appropriate car loan terms. - Home Equity Loans

Interest prices can substantially impact the total cost of the finance, affecting month-to-month payments and the overall amount repaid over the financing term.Effective analysis of repayment terms is vital for borrowers seeking an equity car loan as it straight influences the loan's affordability and financial outcomes. The loan term refers to the length of time over which the debtor is expected to pay back the equity loan.In conclusion, when applying for an equity financing, it is important to think about the kind of financing available, qualification elements, loan-to-value ratio, rate of interest prices and costs, and settlement terms.

Report this page